A Rocky Start for the Stock Market in 2025

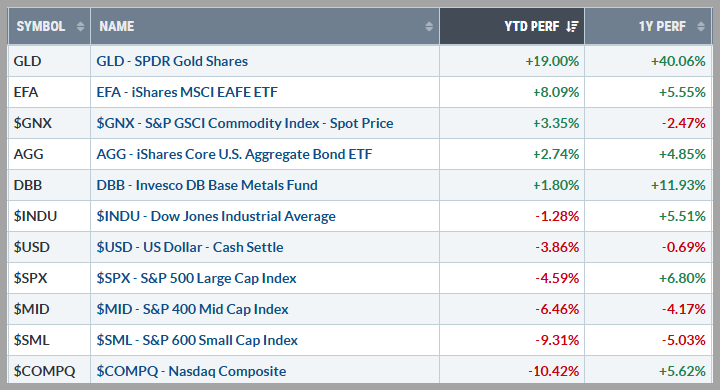

The first quarter of 2025 was a tough one for the stock market, with major indexes experiencing notable drops. The S&P 500 fell about 4.6%, while the Nasdaq took a bigger hit, dropping around 10.4%, largely due to struggles in the tech sector. The Dow Jones held up a little better, slipping only about 1.3% since the start of the year.

Much of this downturn was driven by new tariffs imposed by President Trump on key industries like aluminum, steel, and automobiles. These trade policies have sparked concerns about a slowing economy and rising inflation, fears that seem to have put a real damper on consumer confidence. In fact, consumer sentiment is at some of its lowest levels in years, a trend we’ve typically only seen during major market downturns. The silver lining? Historically, when things look this bad, a rebound may not be far behind.

That said, the economy itself doesn’t appear to be in as rough a shape as market sentiment might suggest. While GDP estimates were lowered, they’re still positive, and the job market remains relatively strong with steady hiring. People and businesses are still spending, corporate profits are up for the most part, and inflation has been easing.

Meanwhile, the Federal Reserve chose to keep interest rates steady at their March meeting and doesn’t seem to see a recession on the horizon just yet. They expect inflation to continue cooling and have hinted at two potential rate cuts later this year depending on how trade policies and government spending play out. On the employment front, they don’t anticipate a surge in job losses, which is another reassuring sign.

Intermarket Trends: Signs of Optimism Amid Uncertainty

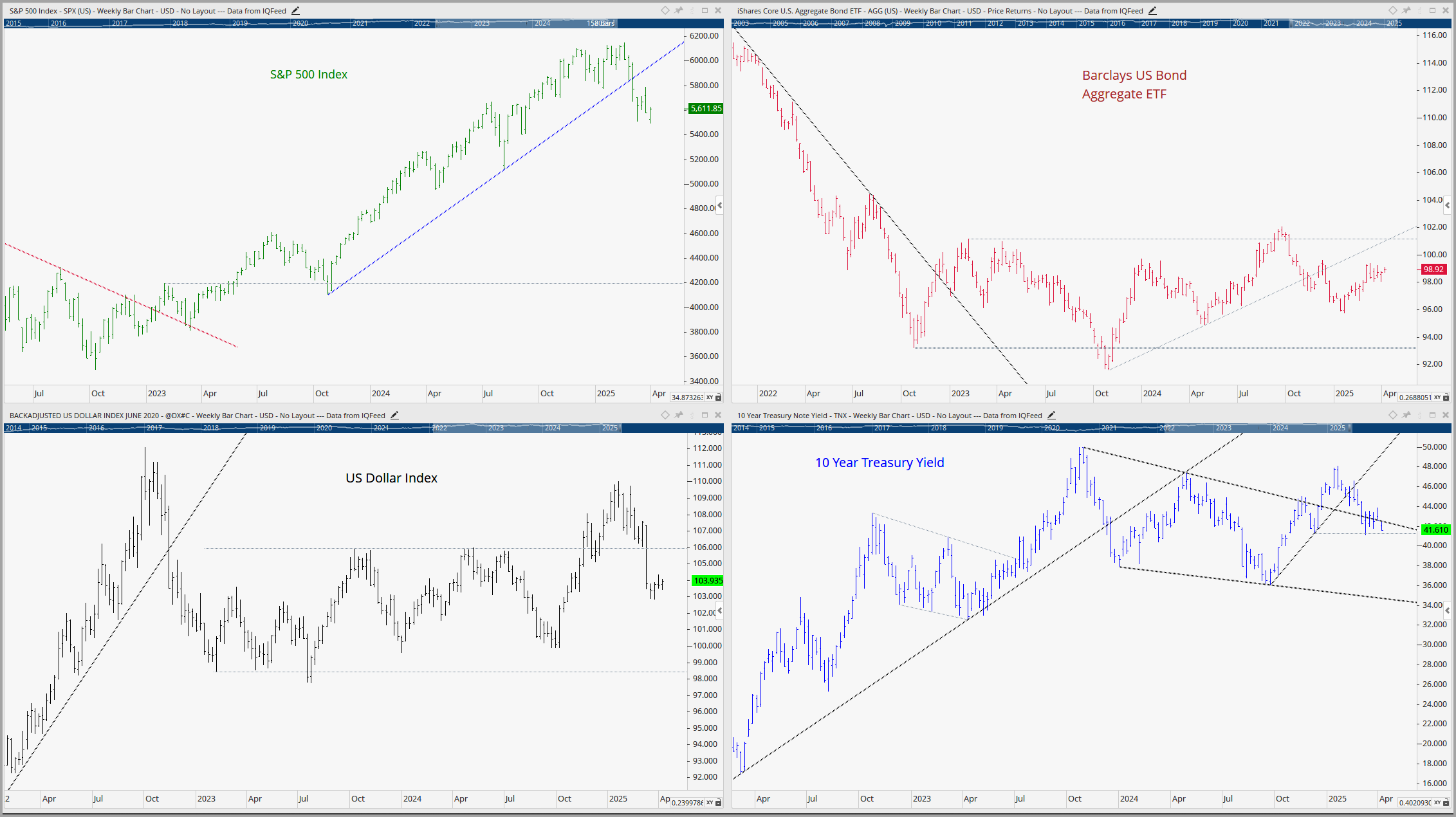

There have been some interesting shifts in the financial markets recently. Long-term interest rates have eased a bit, with the 10-year Treasury yield dropping by 0.5% to around 4.1%. At the same time, the U.S. dollar has pulled back by about 3.5%. Both of these trends are generally good news for the stock market.

Another notable development is the surge in copper prices, which is generally seen as a key indicator of economic growth. “Dr. Copper,” as Wall Street calls it, has jumped more than 25% this year, hinting at potential underlying economic strength. At the same time, the bond market isn’t showing any major warning signs. Credit spreads, or the difference in yields between low-risk U.S. Treasuries and higher-risk bonds, are still near historic lows. This matters because when bond investors anticipate trouble, they demand higher yields on riskier bonds. Right now, that’s not happening, which suggests that “Smart Money” isn’t signaling major concerns.

Meanwhile, gold did hit fresh record highs this week as the growing uncertainty has pushed a fear bid into the precious metal.

Source: Stockcharts.com

While markets have been volatile, the stability in credit spreads and solid economic data suggest that underlying financial conditions remain sound. Consumer confidence has taken a hit due to uncertainty surrounding tariff announcements and government cost-cutting initiatives. When uncertainty is high, markets tend to react with increased volatility, as investors and business leaders struggle to plan for the future. However, history has shown that once there is more clarity on policy direction, confidence may stabilize, and markets often find their footing again.

Most of the stock market’s losses in Q1 have come from the technology and consumer discretionary sectors, which together currently make up approximately 40% of the S&P 500. These sectors had been trading at high valuations, so a pullback wasn’t entirely unexpected. Behind the scenes, though, money has been shifting into other areas like financials, energy, and more defensive sectors such as utilities, healthcare, and consumer staples.

A closer look at the Dow Jones Industrial Average, which is less exposed to tech and consumer discretionary stocks, shows that the broader market isn’t as weak as the S&P 500 and Nasdaq suggest. This kind of sector rotation, where leadership expands beyond just a few high-growth areas, can actually be a healthy sign. If sentiment improves, this “broadening effect” could set the stage for a more stable and sustainable market recovery once investors gain more certainty around governmental policy shifts.

Source: Optuma with DTN IQ data

The Week Ahead:

All eyes are on the White House’s April 2nd tariff announcement, as investors await details on which goods will be affected and how impacted countries may respond. While uncertainty remains, we do know that, as of this writing, a 25% tariff is set to be imposed on imports from any nation purchasing oil or gasoline from Venezuela, along with a 25% tariff on imported automobiles. Treasury Secretary Scott Bessent has hinted that some tariffs may be adjusted or negotiated down, but markets remain on edge. Given that imports currently only make up about 15% of U.S. GDP, the overall economic impact may not be as severe as feared. If the worst-case scenario doesn’t materialize, markets could see an upside surprise.

Beyond tariffs, economic data will also play a big role this week. The Chicago PMI came in stronger than expected, while the Dallas Fed Manufacturing Survey showed mixed results. Investors will closely watch today’s reports on PMI Manufacturing, ISM Manufacturing, Construction Spending, and JOLTS job openings. However, the most anticipated release is Friday’s Employment Situation report, with forecasts expecting the unemployment rate to tick up slightly to 4.2% and 131,000 new jobs to be created. How these numbers shape up could set the tone for market sentiment in the days ahead.

Current Observations

Economic Growth: The economy appears to be growing at a moderate pace, not too hot. The GDP in the United States expanded 2.5% year-on-year in the fourth quarter of 2024 , slowing slightly form a 2.7% rise in the previous period. GDP Annual Growth Rate in the United States averaged 3.16 percent from 1948 until 2024.

(source: U.S. Bureau of Economic Analysis)

Inflation: Inflation has been cooling over the past year but appears to be a little “sticky” in recent months. The annual inflation rate in the US edged up to 3% in January 2025, compared to 2.9% in December 2024, and above market forecasts of 2.9%, indicating stalled progress in curbing inflation. This marks the fourth increase in inflation in recent months, however Core Personal Consumption Expenditures (PCE) index, the Federal Reserve’s preferred inflation measure, recently eased to 2.6% from 2.8% a month earlier.

(source: U.S. Bureau of Labor Statistics)

Employment: The jobs market remains robust despite the recent rise in unemployment from historically low levels.The US economy added 151K jobs in February 2025, up from a downwardly revised 125K in January and compared to forecasts of 160K. The U.S. unemployment rate rose to 4.1% in February 2025, up from 4.0% in January and slightly exceeding market expectations of 4.0%

(source: U.S. Bureau of Labor Statistics)

Monetary Policy: The Fed kept the federal funds rate unchanged at 4.25%-4.5% during its March 2025 meeting, extending the pause in its rate-cut cycle that began in January, and in line with expectations. Policymakers noted that uncertainty around the economic outlook has increased but still anticipate reducing interest rates by around 50 bps this year, the same as in the December projection.

(source: Federal Reserve)

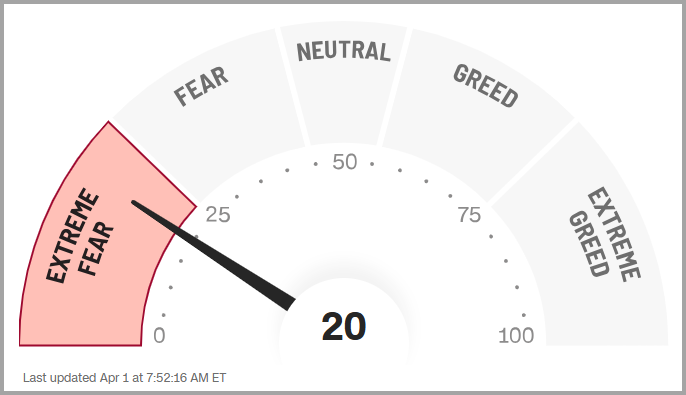

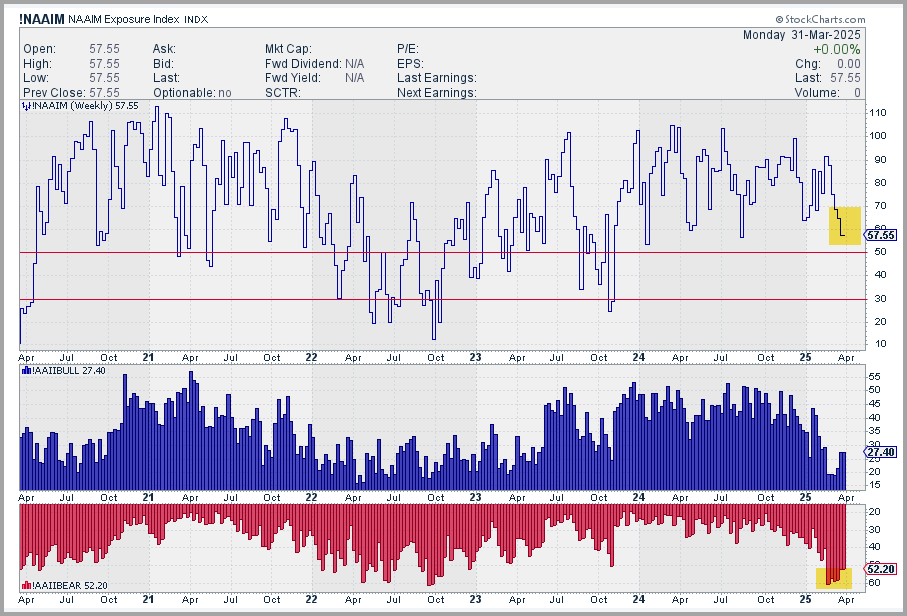

Sentiment: Retail Investor optimism has been waning over the past few weeks. According to AAII, retail investors have become extremely bearish and active money managers look to be following suit. The CNN Fear & Greed index, which measures seven different aspects of market behavior to gauge the “mood” of the stock market, shows that overall, investors are currently extremely fearful. These conditions are typically seen after longer duration bear markets and often signal a “washout”.

Source: https://www.stockcharts.com

Volatility & Speculative Demand: The VIX (CBOE Volatility Index), which is known to be Wall Street’s fear gauge, is trading at lofty levels, indicating investors are on edge. High-yield (or “junk”) bond credit spreads have begun to rise from very low levels and deserve careful monitoring going forward.

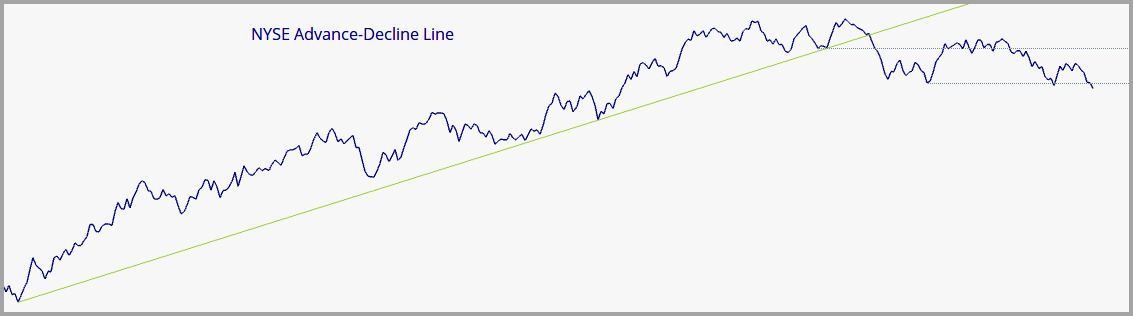

Breadth & Technicals

There has been a major shift in market breadth over the past quarter as stocks have sold off. The chart below shows the upward trend of expanding breadth, broke its upward trendline in mid-December and has been wavering ever since. A break below the recently established lows could spell more trouble to come for the equity markets.

Source: Optuma with DTN IQ data

Tying it all together:

Investor optimism, which had been lifted by easing inflation, potential interest rate cuts, and solid economic growth, has taken a hit recently. Much of this seems tied to uncertainty around the new administration’s tariff policies and budget cuts. Adding to the unease, recent economic “surveys” have hinted at a possible slowdown—but it’s important to remember that these surveys reflect sentiment more than hard facts.

In March, the Federal Reserve reassured investors that it’s keeping a close eye on the economy and is ready to step in if recession risks grow. Here’s what they emphasized:

- They don’t expect a recession, despite signs of slower growth.

- Rate cuts are still on track, likely starting later this year.

- Inflation is expected to ease gradually over time.

- The job market may cool slightly, but a major spike in unemployment isn’t expected.

With markets in what we call “oversold” territory (meaning they’ve dropped a good bit in a short period), the Fed’s supportive stance could help fuel a short-term bounce. However, since they’re staying on the sidelines for now, trade and tariff news will likely continue to drive volatility. Until we get clearer policies and stronger economic data, it’s going to be tough to fully trust any market rally despite recent strong earnings trends.

For now, defensive sectors, value, and low-volatility stocks have held up well, while bond prices have benefitted from falling interest rates — a prime example of how tactically managing (such as we aim to do) a diversified portfolio can endeavor to help investors navigate uncertain times with less exposure to daily market swings.

Stay patient, stay vigilant, stay diversified. Historically, times like these tend to come and go, often providing an opportunity for those who keep an eye on the bigger picture.

Please feel free to share these commentaries and, should you have any questions regarding your current strategy or the markets in general, please reach out to your CIAS Investment Adviser Representative.

Edward J. Sabo

Chief Investment Officer

Capital Investment Advisory Services, LLC

Important Disclosures:

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The statements contained herein are solely based upon the opinions of Edward J. Sabo and the data available at the time of publication of this report, and there is no assurance that any predicted or implied results will actually occur. Information was obtained from third-party sources, which are believed to be reliable, but are not guaranteed as to their accuracy or completeness.

The actual characteristics with respect to any particular client account will vary based on a number of factors including but not limited to: (i) the size of the account; (ii) investment restrictions applicable to the account, if any; and (iii) market exigencies at the time of investment. Capital Investment Advisory Services, LLC (CIAS) reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. The information provided in this report should not be considered a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed may not represent an account’s entire portfolio and in the aggregate may represent only a small percentage of an account’s portfolio holdings. It should not be assumed that any of the securities transactions, holdings or sectors discussed were or will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein.

CIAS is a registered investment advisor. More information about the advisor, including its investment strategies and objectives, can be obtained by visiting www.capital-invest.com. A copy of CIAS’s disclosure statement (Part 2 of Form ADV) is available, without charge, upon request. Our Form ADV contains information regarding our Firm’s business practices and the backgrounds of our key personnel. Please contact us at (919) 831-2370 if you would like to receive this information.

Capital Investment Advisory Services, LLC

100 E. Six Forks Road, Ste. 200; Raleigh, North Carolina 27609

Securities offered through Capital Investment Group, Inc. & Capital Investment Brokerage, Inc.

100 East Six Forks Road; Raleigh, North Carolina 27609

Members FINRA and SIPC